Sixteen Strategies Failed Our Gates. The Four Best Losers, Combined, Passed Everything.

We tested 16 published trading strategies on real tick data. Four kept a real edge but failed our quality bar alone. At pre-registered weights, together, they pass all 14 gates.

Since we started this project we have put sixteen published trading strategies through the same pipeline: real Dukascopy tick data, commission and swap included, optimization only on 2019-2022, one shot at the held-out 2022-2026 window, and a set of quality gates that nothing had ever fully passed. Thirteen strategies died. Their write-ups are all on this site.

Four survived with a real out-of-sample edge and still failed. Each one fell at a different hurdle:

| survivor | family | OOS profit factor | max drawdown | why it failed alone |

|---|---|---|---|---|

| Gotobi Tokyo fix | seasonality | 1.36 | 7.0% | kept only 67% of its in-sample PF, bar is 70% |

| WMR fix reversal | mean reversion | 1.23 | 2.2% | real, but pays ~0.7% a year |

| Asian range breakout | session breakout | 1.16 | 23.7% | drawdown past our 20% cap |

| BTC Donchian trend | trend | 1.12 | 25.2% | PF, drawdown and Sharpe all just under |

Four real edges, four rejections. That is either a very expensive pile of almosts, or one untested idea: what if the unit of judgment is wrong?

The oldest idea in finance, applied to our own rejects

A seasonality edge on USD/JPY, a fix-window fade on GBP/USD, a session breakout, and a crypto trend follower have no business losing money on the same days. We measured it: the average pairwise correlation of their daily P&L streams is -0.01. Effectively zero. Four independent coin flips, each slightly biased in our favor.

Diversification is the oldest free lunch in finance, the math has been known for seventy years. What is usually missing is the honesty part, because a portfolio assembled AFTER you have seen the results is just curve fitting with extra steps. So we wrote the rules down first:

- Universe by rule, not by choice. Every strategy whose out-of-sample edge held, automatically. No cherry-picking which rejects to include.

- Weights from in-sample data only. Volatility parity computed on the 2019-2022 window, frozen before any combined curve existed: WMR fix 54.1%, gotobi 38.1%, BTC Donchian 4.2%, range breakout 3.6%.

- One shot. No re-weighting, no swaps, no second attempt after seeing the out-of-sample result.

- The benchmark formula fixed in advance, so we could not pick a flattering baseline after the fact.

What came out

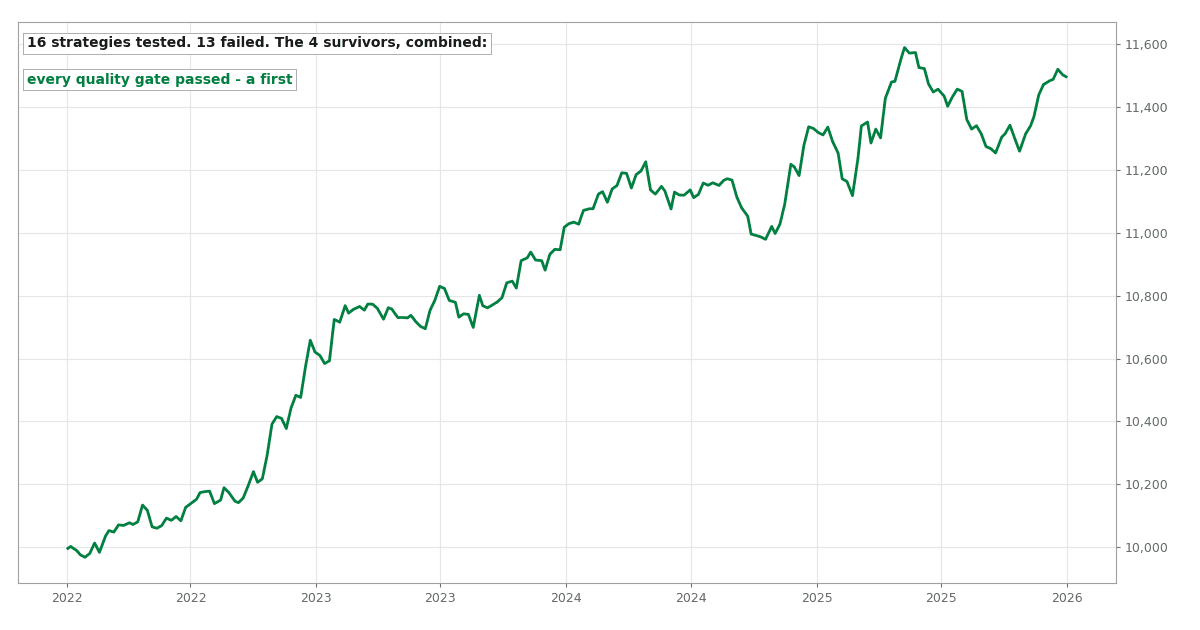

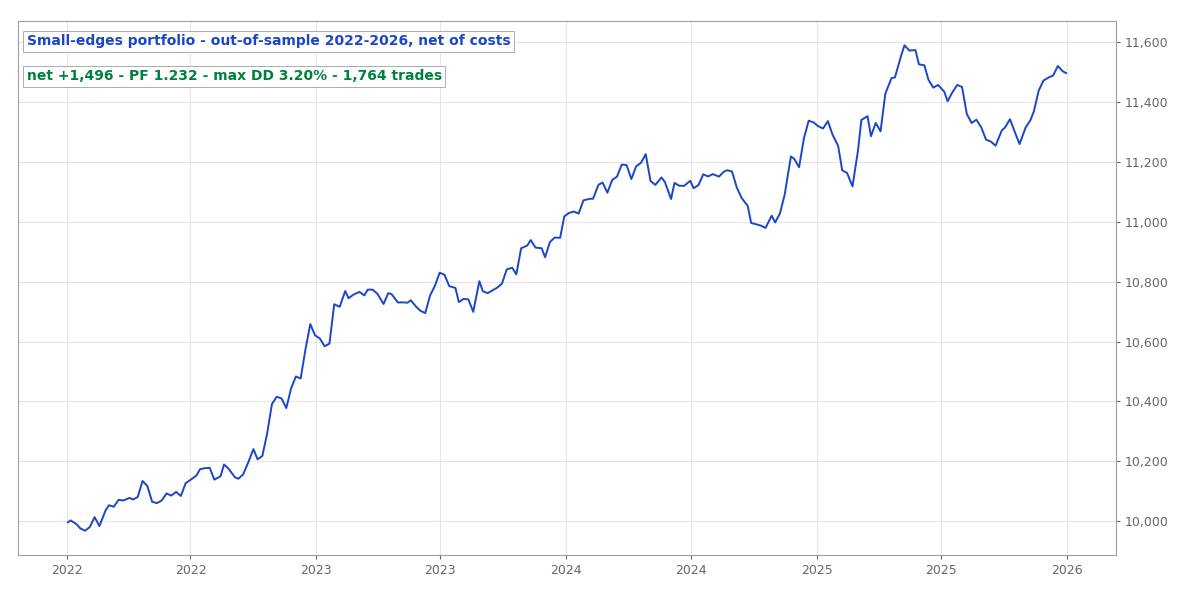

The combined out-of-sample equity curve, 2022-2026, net of modeled costs.

The combined out-of-sample equity curve, 2022-2026, net of modeled costs.

Net profit factor 1.232, with 87% retention from in-sample. Profitable in all four out-of-sample years. Still profitable with commission stressed from $3.50 to $8.50 a side. 1,764 trades.

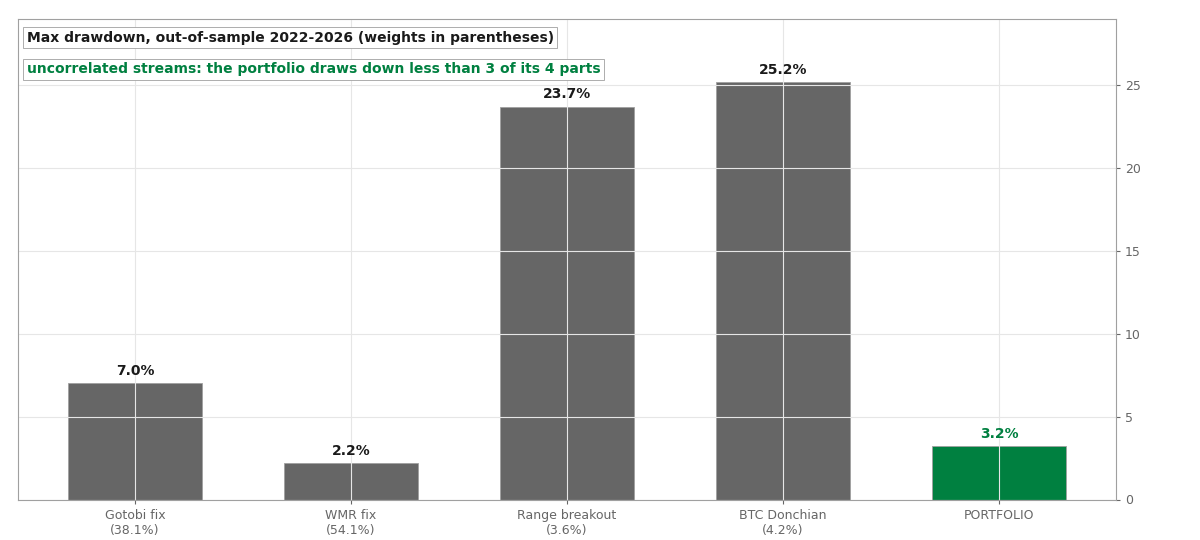

The drawdown chart is the whole argument in one picture:

Max drawdown by component and for the combined portfolio, out-of-sample.

Max drawdown by component and for the combined portfolio, out-of-sample.

Two components drew down 24-25% on their own. The combined book never lost more than 3.2% from a peak, because the four streams take their losses at different times. Nothing was hedged or timed; the near-zero correlation did all of the work.

To check how much of this is luck, we replayed the 1,764 trades ten thousand times, resampled and reshuffled. The bootstrap puts the profit factor between 1.05 and 1.44, with a 0.4% probability the whole window loses money. Explore it yourself:

Each run reshuffles the 283 out-of-sample trades, drawing them with replacement, and totals the result. The blue line is what actually happened; the shaded band left of zero is every run that ended in the red.

And the baseline question: against a weight-blended mix of buy-and-hold and naive momentum on the same symbols, the portfolio delivered 3.9 times the risk-adjusted return. That makes it fourteen gates out of fourteen, which no strategy on this site had ever managed.

The caveat we wrote down before we knew the answer

This is the part most publishers would bury, so it goes in bold instead: the four components were selected because they survived out-of-sample. The combined curve is computed on data every component had already been judged on. This study shows how known edges combine. It is not untouched holdout validation, and no amount of gate-passing makes it one. We pre-registered that sentence along with the weights.

There is only one exam that cannot be studied for, and this portfolio's components are sitting it right now: two of the four are already running live on a demo account, every trade published on our forward test tracker as it closes. The headline return is modest by construction, roughly 3.6% a year at these conservative sum-to-one weights, and leverage is a separate decision we are not making here. The value here is the shape rather than the size: four small honest edges, measured the hard way, adding up to one steady one.

Sixteen strategies in, the graveyard finally produced something better than lessons.