The 9:30 Opening-Range Breakout Is Just Long the Market in Disguise

Everyone posts the 9:30 candle. We tested it on three years of 1-minute data for all three US indices, in-sample only, before writing a line of EA code. A close beyond the opening range doesn't continue in either direction, on any of them. The only positive drift is being long a market that was rising.

The opening-range breakout is one of the most-posted day-trading strategies on the internet. Mark the high and low of the first few minutes after the 9:30 open, wait for a candle to close beyond that range, and ride the move. The "9:30 candle," the "15-minute ORB," the NQ open. It has a real paper trail too: Zarattini, Barbon and Aziz put a 5-minute version through 7,000 US stocks from 2016 to 2023 and reported a 33% annualized alpha, and an older study found the same shape on index futures across five countries.

So we tested it on the markets the retail crowd actually trades it on: the three big US indices, the Nasdaq-100, the S&P 500 and the Dow. Three years of one-minute data, 2019 to 2021, our in-sample window. And we measured it the cheap way first, before writing a single line of EA code: if the effect isn't even there in the raw data, there's nothing to automate.

The rule was the standard one. Mark the opening range as the first 15 or 30 minutes after the 9:30 New York open. When a 15-minute bar closes beyond the range, that's the breakout. Then we asked the only question that matters before targets and stops enter the picture: after a close beyond the range, does price actually keep going?

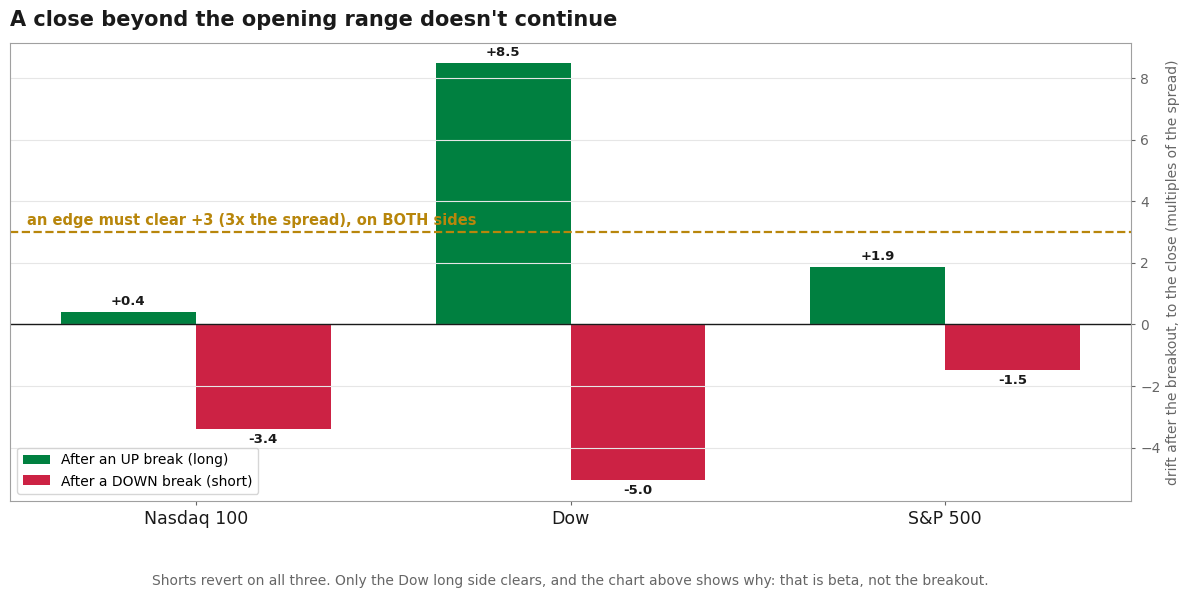

The breakout doesn't continue

Drift after the breakout, held to the close, measured in multiples of each index's spread so the three are comparable. An edge needs to clear +3 on both sides. Shorts revert on all three; only the Dow long side clears, for a reason the next chart makes obvious.

Drift after the breakout, held to the close, measured in multiples of each index's spread so the three are comparable. An edge needs to clear +3 on both sides. Shorts revert on all three; only the Dow long side clears, for a reason the next chart makes obvious.

Over roughly 700 breakouts per index in three years, the answer is no, and it's the same answer on all three.

After an upside break, price barely drifts further by the close. After a downside break, it doesn't continue at all. It reverts. On the Nasdaq, downside breaks gave back about 5 points into the close; on the Dow, about 5; on the S&P, about 1. An edge worth automating should clear roughly three times the spread, on both sides, because the range doesn't know which way the news broke. Not one index clears it short. A close beyond the opening range simply carries no information about where the rest of the day goes.

There is one green bar that pokes above the line: the Dow's long side. Hold that thought, because it isn't what it looks like.

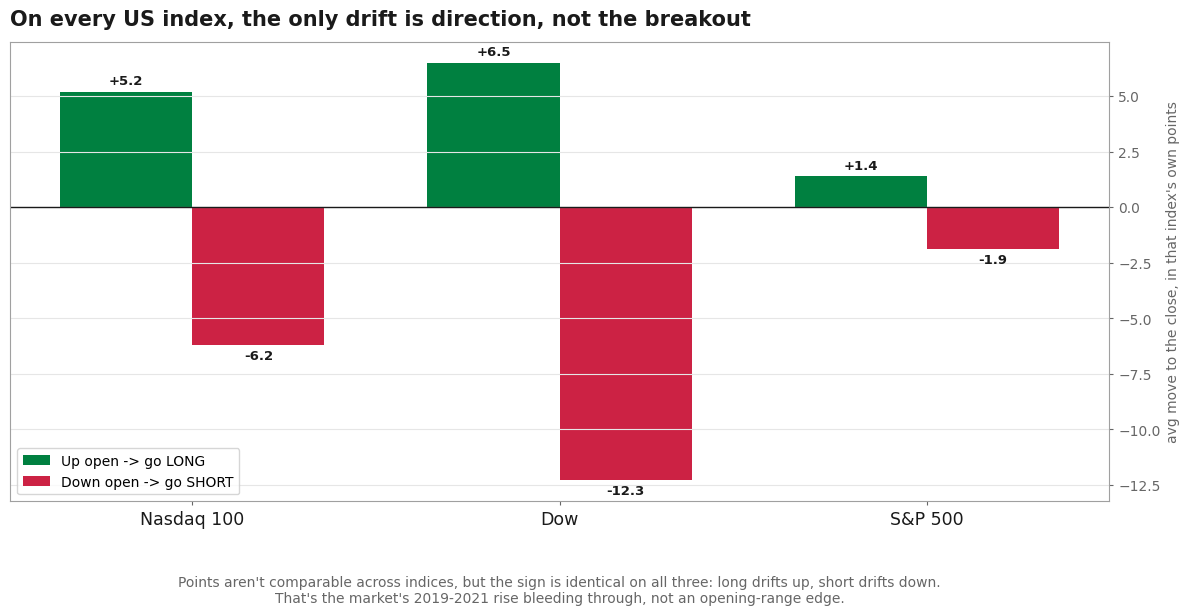

The only thing that "works" is being long the market

Here is the number that explains every viral ORB backtest at once, on all three indices at the same time.

On the Nasdaq, the Dow and the S&P, buying after an up open makes money and shorting after a down open loses it. The sign is identical on all three, which is the tell: this is market direction, not an opening-range signal.

On the Nasdaq, the Dow and the S&P, buying after an up open makes money and shorting after a down open loses it. The sign is identical on all three, which is the tell: this is market direction, not an opening-range signal.

Buy after the opening range closes up, hold to the close, and you make money on every index. Short after it closes down, and you lose on every index. A real opening-range edge would pay on both sides. This one only pays long, and only because all three indices spent 2019 to 2021 going up. The Dow's long side looked like an edge in the first chart for exactly this reason: the Dow trended hard, so buying its up-opens inherited the trend. You are not harvesting an opening-range effect. You are long the index in a bull market, with extra steps.

So where do the viral numbers come from?

If the directional edge isn't there, why does every ORB backtest look like a rocket? Four reasons, and none of them is the breakout.

The first is the payoff geometry. Put the stop at the other end of the range and a target two ranges away, and the simple version turns marginally green. But that is the target doing the work, not the signal. On the Nasdaq it is worth three cents on the dollar risked before commission, and it goes negative once a normal commission is added. It isn't even stable across years: it made money in 2019 and 2021 and lost in 2020. That's a coin flip with the payout rigged by where you place the target, which is exactly what critics of the strategy have said for years.

The other three are how the famous results get their size. Leverage, because a 3x ETF like TQQQ turns a modest edge into a headline 1,484%. Selection, because the academic version only works once you filter down to the handful of "stocks in play" reacting to news that day, not a plain index. And regime, because a long-biased strategy tested through a bull market inherits the bull market. Take those four away and the plain, both-sided, single-index breakout is what we measured on all three US indices: nothing.

Why this negative is worth having

We didn't build an EA. We didn't touch the out-of-sample years. The whole thing was a short script against the raw one-minute files, and it killed the idea for the price of an afternoon. That is the point of measuring existence before building anything: the opening-range breakout is enormously tunable, and if we had gone straight to a full optimizer on one index we would have found a profitable-looking setting, the same way anyone testing two thousand variants finds one by luck.

Running it across all three US indices is what makes the verdict hard to argue with. A single-index result invites the obvious reply, "you just picked the wrong index." Three indices, same answer, closes that door: the breakout doesn't continue on any of them, and the money that shows up is the market rising, not the range breaking. The strategy isn't a scam. It is a real thing that real people trade. But the edge they think they're trading isn't the one paying them. What's paying them is leverage, stock selection, and a rising market. Which is worth knowing before you wire a stop-loss to it.