We Tested the Best-Evidenced Idea in Finance at the Scale a Retail Trader Can Reach

Trend following works because of breadth, say Man Group and AQR: many mediocre streams, one good portfolio. We ran the experiment with the six markets a retail account actually has. 58 of 60 configurations lost money.

Trend following has more evidence behind it than almost anything else in trading. AQR traced it across a century of data. Man Group runs it across 50 to 150 markets and reports both a positive long-run Sharpe and a positive Sharpe in crises. The argument was never that any single market trends reliably. It is that a weak signal, spread across many markets that do not move together, adds up to a strong portfolio.

We had already measured the weak part ourselves. Our BTC Donchian test made money out of sample with a profit factor of 1.12 and got rejected for it. The EURJPY version was marginal. Gold trend failed twice, in two different forms. So we ran the actual experiment: does combining them rescue what each one could not do alone?

The setup, locked before any run

Six markets, which is what a retail MT5 account with good data actually gives us: EUR/USD, GBP/USD, USD/JPY, EUR/JPY, gold and Bitcoin. One Donchian close-channel signal on H4, long and short, ATR stop, channel exit. Five years in sample (2017 to 2022), the 2022 to 2026 window locked away as always.

Three rules went into the spec before we touched the tester, because each one blocks a specific way of fooling ourselves:

- All six markets, no exceptions. Dropping a market after seeing it lose is curve-fitting at the portfolio level.

- One shared parameter set for every market. Per-symbol tuning is where our earlier single-market results got their flattering numbers.

- The unit of judgment is the combined portfolio stream, run through the same gates every strategy faces.

Two pieces of prep work paid for themselves. We repaired a hole in our Bitcoin history first (65.7 million ticks re-imported for 2019 to October 2020, so the test would not run on broken data). And a quick correlation check on simulated streams said the diversification math was genuinely there: average pairwise correlation of 0.12, an effective four markets of independence from the six. The ceiling was real. The question was whether the streams underneath it were good enough.

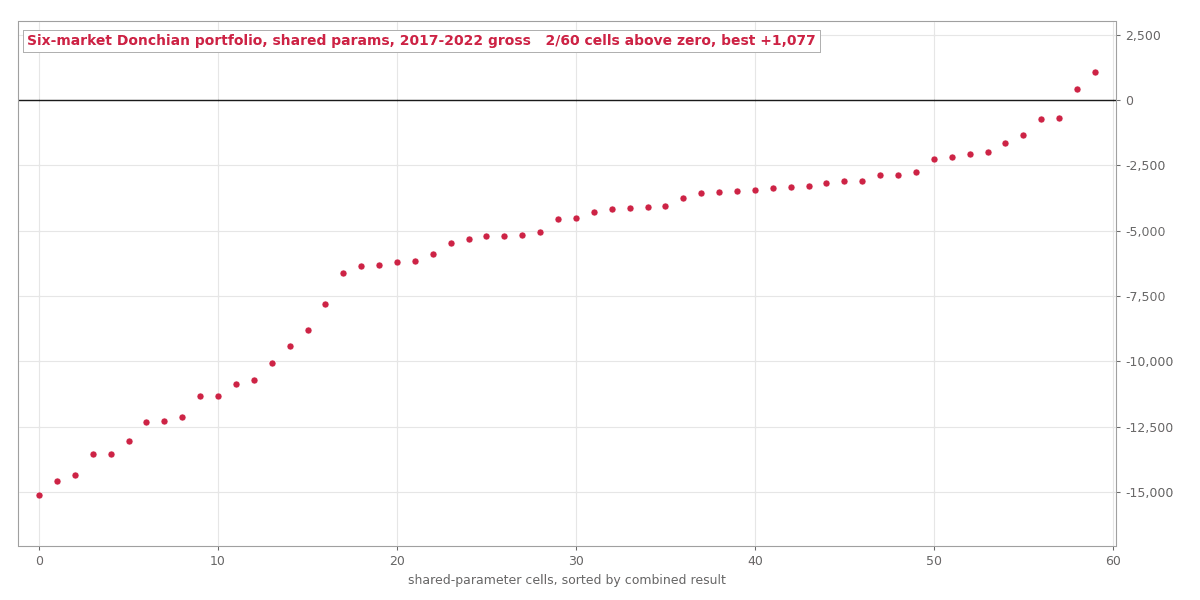

The result

They were not. Across the complete 60-cell grid of shared parameters, summed over all six markets and five years, exactly 2 cells finished above zero. The best of them earned $1,077 across 2,597 trades. That is 41 cents per trade. Not a single cell passed the robustness check that requires its neighboring parameter cells to be healthy too.

The breakdown at the best cell explains the failure better than any theory:

| Market | 5y result | Profit factor |

|---|---|---|

| BTC/USD | +$5,964 | 1.48 |

| EUR/JPY | +$2,270 | 1.11 |

| USD/JPY | +$1,407 | 1.07 |

| EUR/USD | +$416 | 1.02 |

| GBP/USD | −$522 | 0.97 |

| XAU/USD | −$8,457 | 0.23 |

Bitcoin built a house and gold burned it down. With 50 futures markets, one toxic stream is a rounding error. With six, it is a third of the roof.

The obvious question, measured instead of dodged

Anyone looking at that table asks the same thing we did: what if you just drop gold? We measured it, since the analysis was free and the locked window stayed locked. Without gold, 39 of 60 cells go positive and the grid's best cell reaches +$9,534:

The same 60 shared-parameter cells with gold excluded: broadly positive, still thin

The same 60 shared-parameter cells with gold excluded: broadly positive, still thin

Two of those cells even pass the robustness check properly. And it still does not matter, for a reason that has nothing to do with statistics etiquette: the better of those robust cells earns a portfolio profit factor of 1.08, about 1.3% per year. Our gates require 1.30 in sample before a strategy may even attempt the out-of-sample window. This is not a promising variant blocked by a technicality. It is a thin edge blocked by being thin.

The etiquette matters too, so we say it plainly: the exclude-gold portfolio was designed by looking at the results. It survives as a recorded observation in the research notes, not as a strategy.

What we think this means

The institutional evidence for trend following is probably right and probably not available at this scale. The breadth that makes it work is 50-plus genuinely different markets at futures-grade costs. Six retail instruments, four of them currency pairs that share legs with each other, cannot substitute for that, and the shared parameter set exposed how much of our earlier single-market "almost" results came from tuning each market separately.

The experiment also cost us nothing where it counts. Rejected in sample, zero out-of-sample runs consumed, and the locked window is still clean for whatever we test next.

One process note. After the verdict we re-audited the tooling and found a bug in our own selection code: the robustness check was comparing candidate cells against a filtered set of healthy neighbors instead of the full grid. Fixing it made the rejection stronger, not weaker, and the exclude-gold numbers above are from the corrected run. Two audits, two bugs found, two verdicts that survived. We keep doing the audits.

All tested strategies, winners and losers, live on the results page.

Past performance is not indicative of future results. These are backtests with realistic cost assumptions, not live trading records.