We Gave a Trend System Five Years of Sample. It Gave Back a 1.17 Profit Factor.

First run of our pre-registered 5-year slow-trend window: EURJPY channel breakouts are mildly real, never validation-grade, and the filter that helped Bitcoin made the carry cross worse.

After the gold chandelier test, we changed our infrastructure rather than our standards: strategies that trade 30 to 50 times a year can now declare a pre-registered five-year in-sample window (2017 to 2022) instead of three, with every quality gate unchanged. This is the first strategy to use it, and the window did exactly what it was built for. Every one of the 27 grid passes had 280 to 690 trades. Whatever follows is a verdict about quality, not sample size.

The candidate was chosen by an internal question, not an external claim. Our channel-trend mechanism has two data points: real but mediocre on Bitcoin H4 (the one BTC strategy that made money out of sample), dead in gold chop. Hypothesis: the mechanism lives where persistent directional flows exist. EURJPY is the classic carry cross, the strongest flow candidate we have: funding-currency dynamics that grind it up for months and crash it down in days. Donchian close-breakouts, both directions, opposite-channel exits, ATR disaster stop, native asymmetric swaps included.

Real-ish, and never good enough

The raw channel grid: 14 of 27 passes gross-profitable, best pass +$4,993 across 688 trades, and a coherent gradient pointing at faster settings, the exact opposite of gold's slower-is-better gradient, which is itself evidence the mechanism responds to each market's flow structure rather than to luck. But the best profit factor anywhere in the grid was 1.17, against our 1.3 gate. The selection tooling refused every pass, correctly.

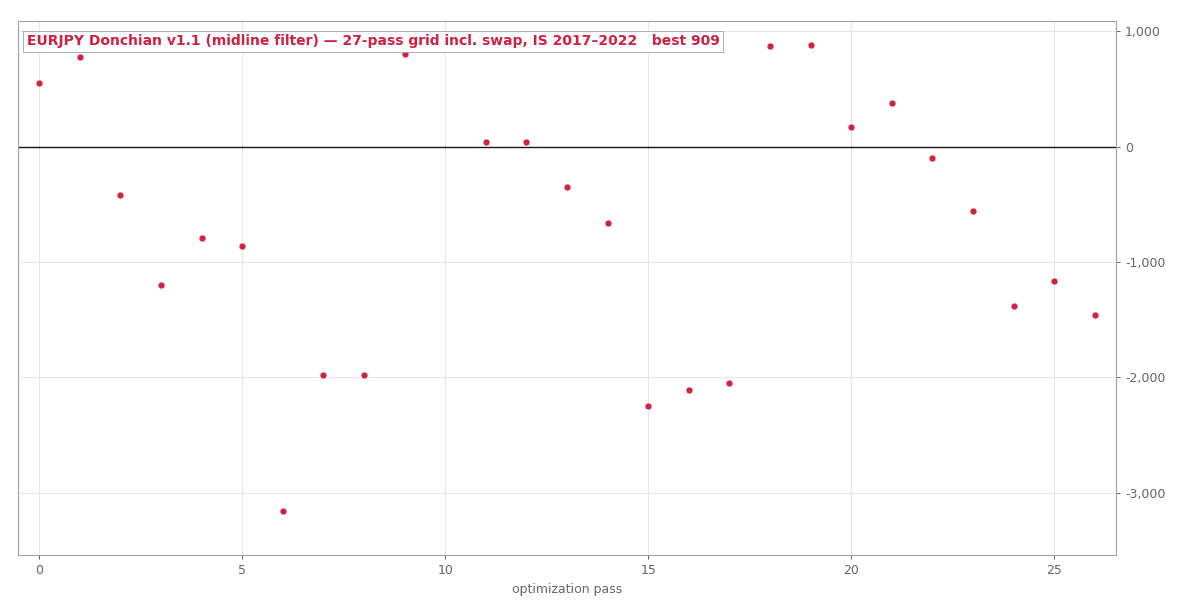

The v1.1 grid, in-sample 2017 to 2022, including swap. Mildly real, never validation-grade.

The v1.1 grid, in-sample 2017 to 2022, including swap. Mildly real, never validation-grade.

We allowed ourselves exactly one pre-registered iteration: our EURJPY spec had deliberately omitted the 50-bar midline regime filter that the Bitcoin version used, so we added it back, expecting it to cut the chop trades and lift the profit factor. It did the opposite. Profitable passes dropped from 14 to 10, the best profit factor fell from 1.17 to 1.10, and the top pass shrank from +$4,993 to +$909. On a carry cross, the trades that pay are often the crash reversals that break out against the prior regime, and a regime filter is a machine for deleting exactly those. The filter turned out to be a bet about the market rather than a property of the mechanism, and it was the wrong bet here.

Where this leaves the trend family

Four data points now: Bitcoin H4 carried out of sample at PF 1.12 with honest retention; EURJPY H4 peaks at 1.17 in sample; gold H4 went 0 for 36; H1 was fatal everywhere we tried it. Single-symbol channel trend on our instruments tops out somewhere between 1.1 and 1.36 and never clears a validation-grade bar. That is the textbook result: trend following earns its Sharpe as a portfolio of dozens of markets, where twenty mediocre PF-1.1 streams with uncorrelated drawdowns become one good one. On a single chart you get what we keep measuring, something real and mediocre that we keep rejecting.

So the family is retired from single-symbol specs in our research priors, and the mechanism's future in this pipeline, if it has one, is the same place our other near-misses went: as one uncorrelated sleeve inside a portfolio, judged by forward testing rather than by another grid.