We Reopened a Closed Case With Better Tools. The Case Stayed Closed.

Month-end rebalancing flow at the London 4pm fix, stacked across four FX pairs with the portfolio tooling we didn't have last time. Best shared-parameter cell over five years: 41 cents a trade.

Our research-rejects ledger is not a graveyard, it is a shopping list. Two of its rows described the same idea: month-end trading around the London 4pm fix, killed both times for trade count. Twelve month-ends a year on one pair can never reach the sample sizes our gates demand, and both rows named the same unblock condition: a framework for stacking thin calendars across several symbols and judging them as one stream.

That framework got built for the trend-following portfolio test. So the idea earned its re-admission, on the rule the ledger exists to enforce: a dead idea comes back only when the thing that killed it has actually changed.

Why month-end, specifically

The flow argument has an unusually solid paper trail. Benchmark-tracked funds and currency hedgers rebalance at month-end and execute at the WM/R fix for tracking reasons. BNY publishes a monthly model of these flows, and banks sell month-end rebalancing forecasts to clients. Evans, whose paper anchored our daily fix study, found the post-fix reversal strongest at exactly these dates. And our own out-of-sample data agreed: the daily-fix strategy's 19 month-end trades carried half its entire profit in 13% of its trades.

The design was pre-registered before any run: fade the pre-fix move on the last one to three business days of the month, on EURUSD, GBPUSD, USDJPY and EURJPY at once, one shared parameter set, verdict rendered on the combined four-pair stream over a five-year in-sample window. One disclosure matters: GBPUSD's out-of-sample window is not virgin for this hypothesis, because the month-end subset of the daily study was already analyzed and published. The other three pairs were untouched.

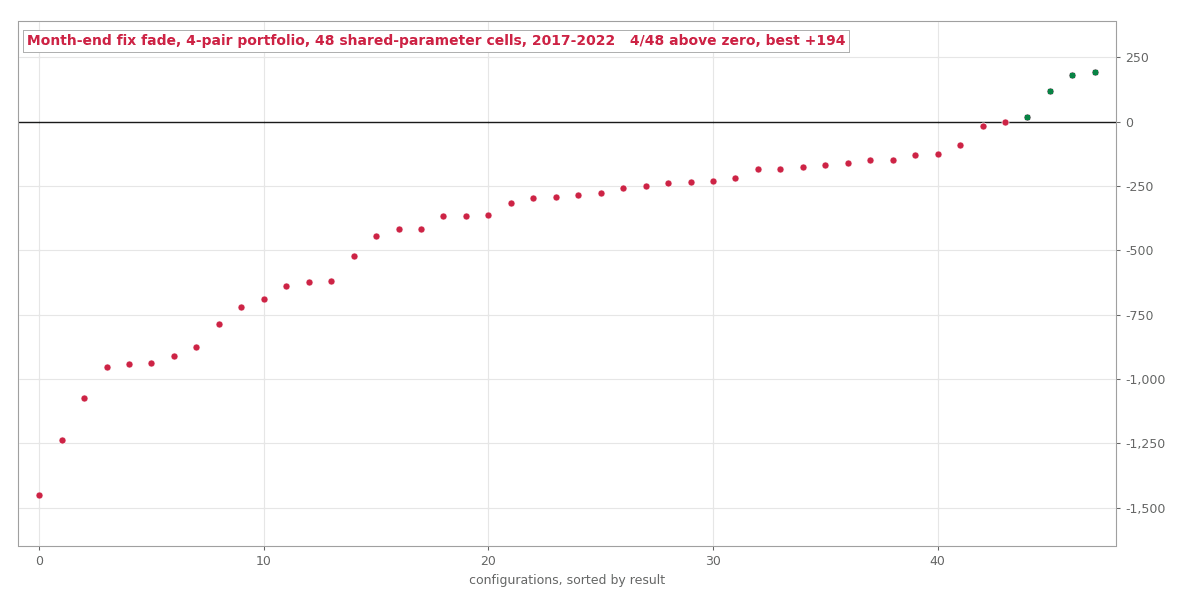

Five years, four pairs, 41 cents

The 48 shared-parameter cells, summed across four pairs, 2017-2022

The 48 shared-parameter cells, summed across four pairs, 2017-2022

Of 48 shared-parameter cells, 4 finished above zero. The best earned $193.86 across 469 trades. Five years, four currency pairs, every month-end the calendar offered, and the best possible configuration paid 41 cents a trade. Readers with long memories will recognize the number: the trend-following portfolio's best cell paid exactly the same 41 cents before we rejected it. No cell was profitable on all four pairs, and no parameter plateau existed anywhere on the surface.

The one structure in the wreckage is worth recording. Cells holding for 15 minutes beat cells holding 30, 45 and 60 minutes, monotonically, across the whole grid. The literature puts the fix reversal's horizon at 1 to 15 minutes, and our surface agrees with the textbook about the shape of an effect it says is too small to own. The 19-trade month-end subset that helped motivate this test now looks like what it probably always was: a small sample doing small-sample things.

Closing the file

This was the fix reversal's third and best-armed attempt in this pipeline. The daily version earned about 0.74% a year on GBPUSD and failed our return-retention gate. The month-end concentration, stacked across four pairs with proper portfolio judgment, earns less than a dollar per trade in sample. The 2015 reform that widened the fixing window did its job, and our research priors now say so explicitly: no more fix-fade variants without a genuinely new mechanism.

The out-of-sample window was never touched. Zero runs consumed, and the re-admission rule that let this test happen also lets it end cleanly: the blocker fell, the question got asked properly, and the answer was no.

All tested strategies, winners and losers, live on the results page.

Past performance is not indicative of future results. These are backtests with realistic cost assumptions, not live trading records.