The Tokyo Fix Anomaly: a Real Edge That Still Didn't Make the Cut

We tested the famous 'gotobi' USDJPY anomaly on 7 years of tick data. It's real, and we still rejected it. Here's the whole story, including the bug we found along the way.

Every so often a trading anomaly comes with an actual paper trail. The gotobi effect is one of them. On Japanese calendar days divisible by 5 (the 5th, 10th, 15th, 20th, 25th and 30th), importers settle dollar invoices, and their banks buy USD ahead of the Tokyo fix at 9:55 JST. That produces buying pressure in USDJPY into the fix on those days. Ito and Yamada documented it in NBER working paper 22820, and arXiv:2301.13204 revisited it in 2023. The flow comes from commerce rather than speculation, which is the usual explanation for why it survived becoming public knowledge.

We picked it as the first test for our research pipeline for practical reasons. The rules are mechanical, the academic sourcing is real, and Japan does not observe daylight saving, so the fix sits at 00:55 UTC all year. No clock ambiguity to argue about later.

The rules we tested

- Trade only gotobi days; when the date lands on a weekend, trade the preceding Friday, per Japanese settlement convention

- Buy USDJPY N hours before the fix. N is the parameter we optimized

- One trade per fix, long only

- Exit at the fix whether the trade is up or down, since the documented pressure ends there

- Fixed stop loss (we explored 15 to 60 pips), risking 1% of equity per trade

How we tested it

Dukascopy tick data, real-tick modeling, $10,000 start, commission included at $3.50 per side per lot. Optimization ran on 2019 to 2022 only. We selected parameter plateaus instead of single best passes, meaning a candidate only counted if its neighbors were profitable too. The 2022 to 2026 window stayed locked until candidates were frozen, and each frozen candidate got exactly one run on it.

Three candidates survived selection, all with net profit factors above 2.0 in sample. Then the out-of-sample window graded them:

| Candidate | In-sample 2019-22 | Out-of-sample 2022-26 | Outcome |

|---|---|---|---|

| Enter 4h before fix | PF 2.10, +$1,295 | PF 0.79, −$1,130 | Collapsed |

| Enter 9h before fix | PF 2.04, +$1,668 | PF 1.36, +$2,171 | Real edge |

| Enter 8h, tight stop | PF 2.10, +$4,125 | PF 1.03, breakeven | No edge after costs |

Two of the three died

All three sat on genuine in-sample plateaus with profitable neighborhoods. The robustness checks passed. The 4-hour entry, which had the best-looking fitness of the lot, still lost money on four years of unseen data:

The 4h-entry candidate out-of-sample: what optimization residue looks like

The 4h-entry candidate out-of-sample: what optimization residue looks like

If we had published the 4h-entry backtest in March 2022 it would have looked spectacular, and it would then have bled for four years. In-sample robustness turns out to be necessary and nowhere near sufficient. We knew that in theory. Now we know it the way you know things that cost you a week.

One candidate held, and we rejected it anyway

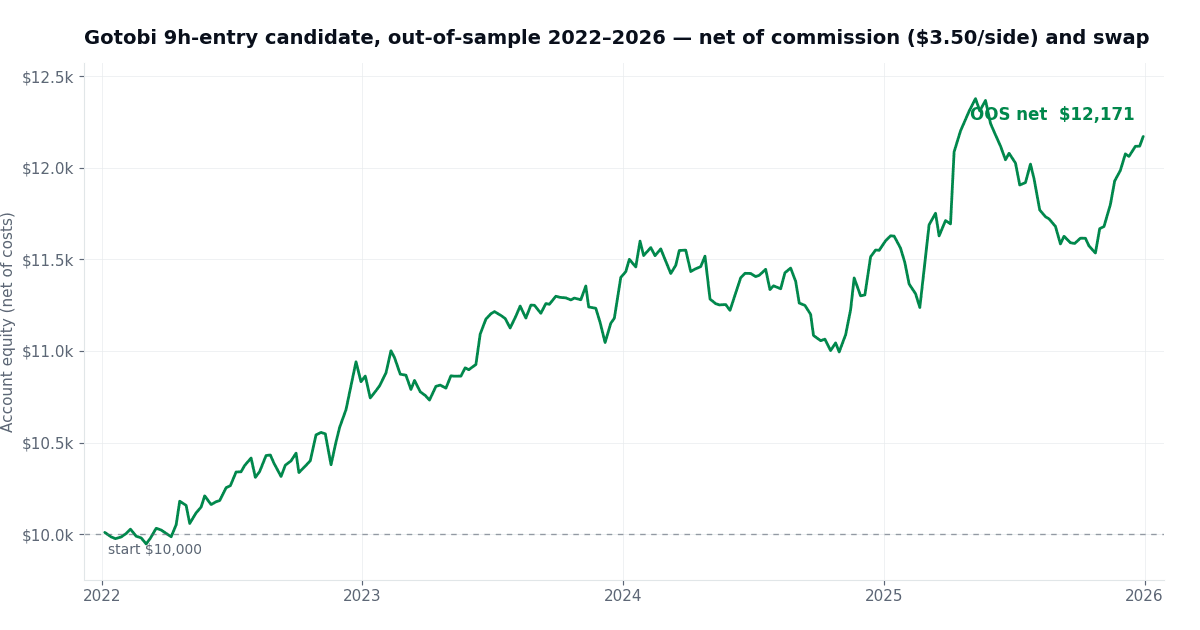

The 9-hours-before-fix entry kept a real edge out of sample: profit factor 1.36 across 283 trades, +21.7% over four years at 1% risk per trade, maximum drawdown of 6.8%. It stayed profitable with commission stressed to $8.50 per side. Part of the return is structural, since long USDJPY collected positive overnight swap the whole time.

The 9h-entry candidate out-of-sample: a real, if modest, edge

The 9h-entry candidate out-of-sample: a real, if modest, edge

So why reject it? Our gates require a candidate to keep at least 70% of its in-sample profit factor out of sample, and this one kept 67%. We sat with that for a while. Lowering a bar after seeing the result is data snooping with a paper trail. Skipping a marginal edge costs nothing; going live on optimization residue costs money.

The surviving configuration moved to a demo forward test instead. Forward data is the one dataset nobody can overfit. If the live demo tracks the out-of-sample profile for a few months, the strategy earns another look.

We ran the survivor 10,000 more times

That 67% retention number is one measurement of one four-year path. Before sending the 9-hour entry to the demo account, we wanted to know how much of the path was a real edge and how much was just the order the trades happened to arrive in. So we resampled it.

Two questions, ten thousand runs each. First, shuffle the 283 out-of-sample trades and draw them with replacement, over and over, and count how often the strategy ends up underwater. Second, keep the exact same trades but deal them in a random order each time, and watch how deep the worst drawdown gets on the runs where the losers bunch up together.

Each run reshuffles the 283 out-of-sample trades, drawing them with replacement, and totals the result. The blue line is what actually happened; the shaded band left of zero is every run that ended in the red.

The edge came through it fine. Only 3.4% of the resamples finished in the red, the median run made about what the real one did, and the real drawdown landed near the middle of the pack at the 67th percentile rather than out on some lucky tail. Its return for the drawdown it took also beat both a buy-and-hold of USDJPY and a plain 12-month momentum rule, by roughly 38%.

None of that saved it. The strategy is sound on every axis we can measure after the fact, and it still missed the one line we drew before we looked: 67% profit-factor retention against a 70% floor. The simulation didn't change the call. It just made us surer the call was about discipline and not about a strategy that was quietly broken.

A note on out-of-sample discipline

We count and disclose every out-of-sample run a strategy consumes (this study used 6 across its full validation cycle), because repeated peeks at the holdout are how people fool themselves. The window is opened once per frozen candidate and the counter is public.

What we took away

The anomaly is real. Every configuration was profitable in sample, net of costs, which matches the literature. The discipline did the useful work, though. It killed two of three "robust" candidates before they could cost anything, and it stopped us from rationalizing the third. A near miss goes to the demo account, not the shredder.

The full interactive report, with equity curves, drawdowns and yearly breakdowns for all three candidates, is on the results page.

Questions about the method? The pipeline (headless MT5 testing, plateau selection, one-shot out-of-sample, cost stress) is being built in public. We're happy to talk shop.