The Backtest Claimed +60% in 11 Months. Ours Found Zero Winning Configurations.

A published gold trading strategy came with a spectacular backtest. We retested the same rules on three years of tick data with real costs and swept the complete parameter grid — all 72 combinations lost money. A case study in why single-period, cost-free backtests can't be trusted.

Larry Williams' volatility breakout is a classic: when price moves a meaningful fraction of yesterday's range away from today's open, that's real order flow, not noise — so go with it. An MQL5 article implemented it for gold and reported the kind of backtest that sells EAs: +60% in 11 months, "steady progression," no extreme drawdowns.

The fine print, easy to miss: the test covered January–November 2025 only — one hand-picked year, on daily bars, in one of gold's great bull runs — and charged zero commission.

Our version of the test

Same rules, implemented faithfully: buy when price closes above

day open + K × yesterday's range (mirror short below), stop at a fraction

of yesterday's range, take-profit at a reward multiple, one trade per day,

flat before the next day's levels.

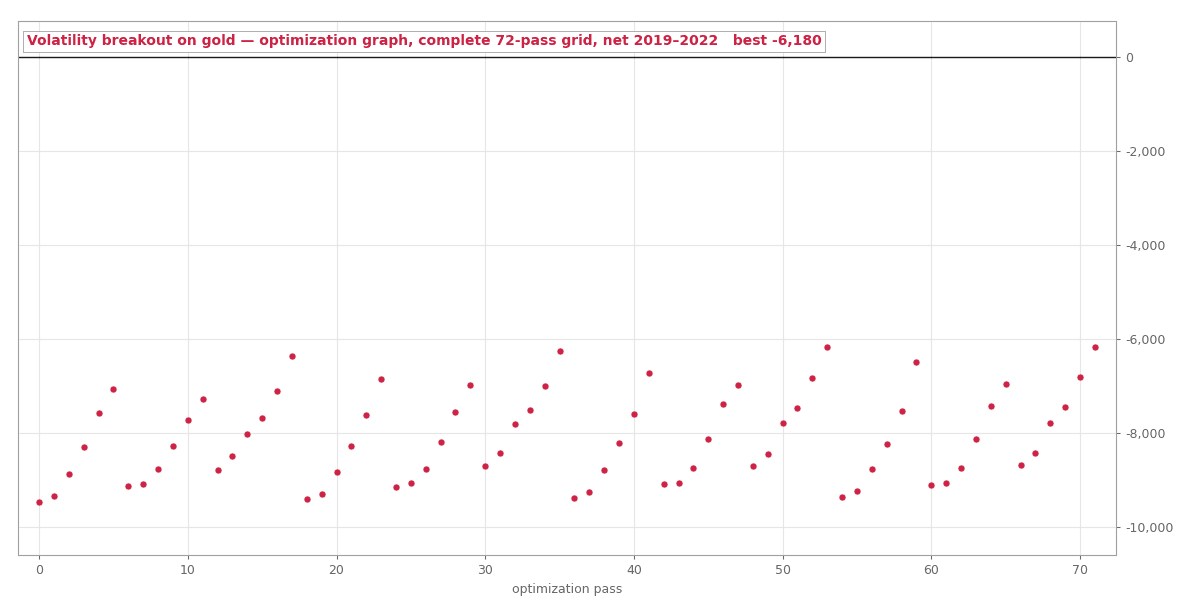

Instead of one lucky year, we ran the complete parameter grid — every combination of breakout multiple (0.3–0.8), stop multiple (0.3–0.7), and reward ratio (2–5), 72 in all — over 2019–2022 on real tick data with commission included. Not a genetic sample that might miss pockets: every single cell of the space.

All 72 lost money. The best combination finished at −$6,180 on $10,000; the worst near −$9,500. There was no corner of the parameter space to rescue, no "with better tuning..." left on the table.

We found a bug in our own test, too

Full disclosure: our first run of this grid had a data-convention bug. On UTC tick data the market's Sunday-evening open creates tiny "Sunday" daily bars (a $3–6 range versus $11–60 for real trading days), and our EA's "yesterday's range" picked those stubs up every Monday — corrupting levels and stops on roughly 20% of trades. A code review caught it, we fixed it (Mondays now use Friday's full range; Sunday stubs never trade), and re-ran the entire grid on clean code. The fix genuinely helped — the best configuration's profit factor rose from 0.28 to 0.42 — but helped is not profitable. Every number in this post is from the clean re-run. Testing rigor has to cut both ways: if we hold vendor backtests to a standard, our own bugs get disclosed and re-run, not quietly patched.

Why the same rules produce opposite backtests

Three differences between their test and ours explain everything:

- Costs. With ~150 trades over three years paying spread and commission on every round turn, the cost drag alone consumes several percent per year before the strategy earns anything.

- The stop sits inside gold's noise. Stops at 0.3–0.7× yesterday's range were routinely hit within minutes; win rates ran near 20% while the ambitious reward targets (2–5× the stop) rarely filled before the 23-hour time exit.

- One year versus three. Gold's 2025 melt-up rewarded any long-biased breakout. Sweep 2019–2022 — chop, crash, rally, range — and the melt-up year's flattery disappears.

None of this makes the source article dishonest; it makes it a single-period, cost-free demonstration, which is what most published backtests are. The retest is what tells you whether there's a strategy underneath the demonstration. Here, there wasn't.

A note on the breakout family

This is our second data point on breakouts. The Asian-session range breakout — a session-anchored cousin of this idea — showed a genuine multi-year edge on USD/JPY while failing on EUR/USD. This daily-open volatility expansion fails on gold outright. The family label tells you almost nothing; the specific mechanism on the specific instrument is the entire question.

Like our RSI(2) gold test, this strategy was rejected at the in-sample stage: nothing survived optimization, so our locked out-of-sample window (2022–2026) was never touched. Total cost of the answer: one afternoon of compute.

All tested strategies — winners and losers — live on the results page.

Past performance is not indicative of future results. These are backtests with realistic cost assumptions, not live trading records.