The Weekend Gap Really Fills. Your Broker Opens Too Late to Catch It.

Published statistics say FX weekend gaps fill 70-86% of the time. Our first backtest produced zero trades, and the reason is the finding: the venue quotes from Sunday evening but only trades from Monday. By then the gap is gone.

The weekend gap fill is one of the oldest pieces of retail forex lore, and unlike most lore it comes with numbers: published statistics put the fill rate at 70 to 86% on EURUSD, depending on direction and lookback. The mechanism is plausible thin-book microstructure. Weekend news forces urgent orders into a Sunday open with no market-maker depth, the price overshoots, and it reverts toward Friday's close once real liquidity returns. We specced a fade across four pairs, pre-registered as a portfolio, and sent it to the tester.

The first smoke test produced zero trades in six months.

Zero trades, and the reason is the finding

The tester journal showed the strategy doing everything right. It detected all eleven qualifying gaps, computed correct entries, stops and targets, and sent the orders. Every single one came back rejected: Market closed.

Our custom symbols carry Dukascopy's real quote timeline, which starts around 21:00 UTC on Sunday. But their trading session, like the trading session of essentially every retail MT5 venue, opens at Monday 00:00 UTC. There are three hours of quotes every week during which no order can exist. So the tradeable version of the strategy enters at the first available price instead, and we measured what those three untradeable hours cost: in the first half of 2021, eight of the eleven gaps had already filled below our smallest threshold before trading opened.

That is the finding. The published fill statistics are true and they are measured on quotes. A retail account lives on the trading session, and the gap fill mostly happens in the hours between the two.

What Monday leaves behind

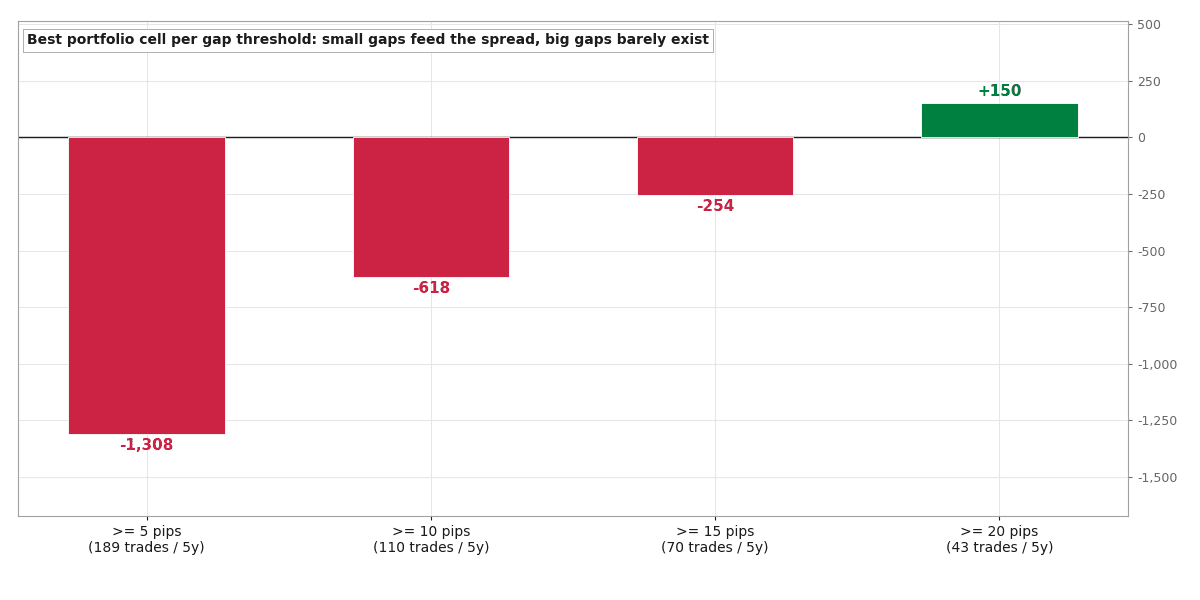

Best portfolio cell per gap threshold: the tradeable leftovers

Best portfolio cell per gap threshold: the tradeable leftovers

What survives to Monday morning is a lose-lose geometry. Small gaps of 5 pips or more still occur often enough to trade, 189 times over five years across the four-pair portfolio, and their best shared-parameter cell lost $1,308, because the Sunday-adjacent spread we measured runs 1.8 to 8.9 pips: the same size as the gaps themselves. Raise the threshold and the losses shrink monotonically until, at 20 pips, the best cell finally turns positive at $150. It gets there on 43 trades in five years across four pairs, a sample below every gate we have and a result the size of noise.

All 48 shared-parameter portfolio cells, 2017-2022

All 48 shared-parameter portfolio cells, 2017-2022

Ten of 48 portfolio cells finished above zero. No plateau, no cell profitable on all four pairs, nothing to select. Rejected in sample, zero out-of-sample runs consumed.

The rule this adds

Our Bitcoin overnight study established that the instrument is part of the strategy: an anomaly your venue's spread exceeds does not exist for you. This test extends the rule one layer down. The instrument's SESSION STRUCTURE is part of the strategy: an anomaly that plays out during hours your venue quotes but does not trade is equally fiction, whatever the statistics say. Both checks now run at spec time, before a line of code gets written.

The lore, for the record, survives intact. The gaps really do fill. The people collecting that fact are the ones who can transact on Sunday evening, and a retail MT5 account is not among them.

All tested strategies, winners and losers, live on the results page.

Past performance is not indicative of future results. These are backtests with realistic cost assumptions, not live trading records.