The Triple-Swap Strategy, Finally Backtested With Real Swaps: the Carry Is Real, the Trade Is Not

Broker folklore says you can collect three nights of USDJPY swap in a few hours of exposure every Wednesday. We modeled real swaps and ran it. The carry paid every week. The strategy lost anyway.

There is a strategy that lives in broker education pages and forum threads and, as far as we can tell, has never been published with an actual backtest: the triple swap. On Wednesday, forex rollover charges three nights of swap at once to cover the weekend value dates. Long USDJPY carries positive swap. So, the folklore goes, buy Wednesday evening, hold across midnight, exit an hour later, and collect three nights of carry for a few hours of market risk.

Nobody backtests it because almost nobody's backtest charges swaps at all. Ours does: the custom symbols in our tester carry the real swap specification, and we verified it by probe before writing a line of the EA: +10.064 points per night on long USDJPY, tripled on Wednesday. About 3 pips of carry per weekly trade, for free. Allegedly.

The carry arrived exactly as advertised

This part of the folklore is true, and we can show it trade by trade. In the smoke test, every Wednesday-crossing hold collected about $9.90 of swap on a 0.34-lot position, which is three nights at the specified rate, to the cent. Across the full in-sample window (2019 to 2022), the frozen candidates collected over a thousand dollars of pure swap each.

In-sample, the strategy looked wonderful in a specific corner: every single configuration entering at 23:00 UTC was profitable, 12 of 12, with profit factors up to 1.85 on real ticks. That unanimity is seductive. It is also exactly the kind of thing our robustness tooling exists to distrust, and it flagged the fragility before we froze anything: no parameter plateau, a cliff at the 22:00 boundary, weak neighborhoods. We froze the top three candidates anyway and sent them to the one-shot out-of-sample window, because that is what the window is for.

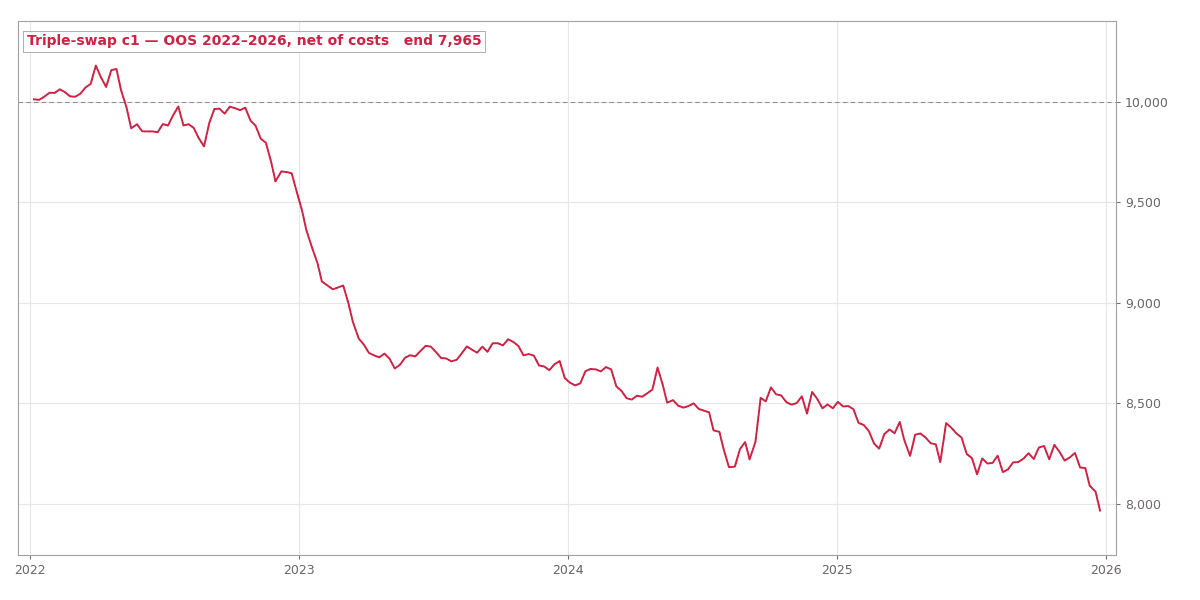

Out-of-sample, the costume comes off

Out-of-sample equity of the top candidate, 2022 to 2026, net of costs. The swap kept arriving every Wednesday while the account lost a fifth of its value.

Out-of-sample equity of the top candidate, 2022 to 2026, net of costs. The swap kept arriving every Wednesday while the account lost a fifth of its value.

All three candidates collapsed: profit factors 0.58 to 0.68, drawdowns up to 38.5%, eight failed gates each. And here is the finding that makes this rejection worth publishing. The swap column stayed positive the whole time. Across 208 out-of-sample Wednesdays the candidates collected $1,305 to $2,010 of carry, exactly on specification. The price leg lost three to five times that.

The in-sample profits were never carry. They were a price drift in the 23:00-to-early-Tokyo window that existed in 2019 to 2021 and inverted when the yen entered its intervention era in 2022. The carry was real in both windows; it was also small enough to be irrelevant. Three pips a week does not pay for hours of USDJPY exposure in a regime where the pair can move a hundred pips overnight.

The in-sample landscape that fooled the grid: every 23:00-entry configuration profitable, everything else flat or negative.

The in-sample landscape that fooled the grid: every 23:00-entry configuration profitable, everything else flat or negative.

What we take from it

First, a definitional point we now apply to every carry idea: a swap-harvesting scheme with market exposure is a regime bet wearing a carry costume. The costume is verifiable; the bet underneath is what you actually own.

Second, the folklore has a second, quieter flaw nobody mentions: real brokers roll at New York 5pm, not at UTC midnight, so the exposure window a live trader holds is a different market session from anything a UTC-clock backtest models. Our strategy failed before that subtlety even mattered, but it means even a positive result here would not have transferred without a second test.

Third, the tooling earned its keep twice: native swap modeling made the carry claim testable at all, and the plateau check called the fragility before the out-of-sample window confirmed it. When the robustness warning and a beautiful in-sample table disagree, believe the warning.

Anyone running the triple swap live since 2022 has been collecting their three pips every Wednesday while their account bled out around it. That is the cruelest kind of losing strategy: the part you can see working really is working.