Half of a Journal of Finance Effect Is Still Real. It Pays Less Than the Commission.

The FX session cycle is documented in top journals: currencies fall during their own trading hours. We measured it on EURUSD tick data. The European leg still works, at 0.75 pips a trade. Costs are 0.7.

This one had the best paper trail of anything we have tested. Breedon and Ranaldo documented it in the Journal of Money, Credit and Banking in 2013: currencies systematically depreciate during their own trading hours, because local participants are net buyers of foreign exchange during their business day, and the pattern shows up in order flow. A 2024 Journal of Finance paper by Krohn confirmed the around-the-clock cycle. Practitioner replications exist, and they come with a warning we will get back to: the edge per trade is a handful of pips, and it is very sensitive to costs.

For EURUSD the recipe is mechanical: short through European hours (EUR falling during Europe's day), flip long at midday, ride the US hours (USD falling during America's day), flat by 21:00 UTC, never hold overnight. Two trades per weekday, about 520 per year. We optimized only the session boundaries and the disaster stop: 27 combinations.

Zero of 27, and then the interesting part

The full package lost in every configuration: profit factors 0.87 to 0.97 across roughly 1,558 trades per pass, best corner minus $1,676. But before running the grid we had pre-registered a decomposition: split every trade by leg and look at the two halves of the cycle separately. That split is the finding.

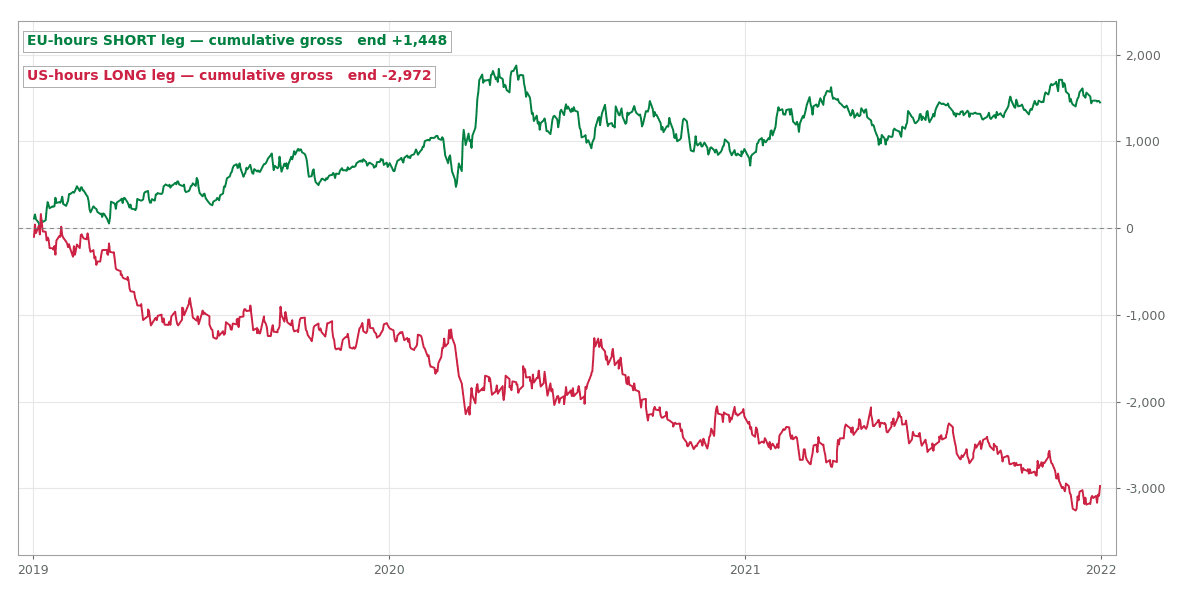

Cumulative gross price P&L per leg, 2019 to 2022. The European-hours short leg grinds steadily to +$1,448; the US-hours long leg bleeds to −$2,972.

Cumulative gross price P&L per leg, 2019 to 2022. The European-hours short leg grinds steadily to +$1,448; the US-hours long leg bleeds to −$2,972.

The European-hours short leg is genuinely, persistently profitable: +$1,447.59 gross across 780 trades, about 0.75 pips per trade, earned in a nearly straight line across three years. The academic effect is not dead. The US-hours long leg is inverted: minus $2,971.92 across 778 trades, which fits the regime; the documented US-hours EUR appreciation ran head-first into the 2021-onward dollar strength.

The arithmetic that ends it

So drop the losing leg and trade the European short alone? We had pre-registered exactly that as the v2 hypothesis, and then did not even need to run it. At our cost model, one round trip costs about 0.7 pips in commission, with spread already living in the fills. The surviving leg earns 0.75 pips gross. Net expectancy: roughly 0.05 pips per trade, a profit factor within noise of 1.0, against a validation gate of 1.3. There is no session boundary, stop width, or leg toggle that turns five hundredths of a pip into a strategy.

The replication literature warned about precisely this, and now we have the measurement: the session cycle is an order-flow fact, not a retail trade. Institutions netting flows at size can harvest it; an account paying $7 per lot round trip cannot.

An audit footnote that made the rejection stronger

Our post-run bug check found something embarrassing and useful: 82 of the 1,558 trades never got their 21:00 exit, because in US summer DST the FX week ends at exactly 21:00 UTC on Friday. No tick at or after the exit time means no exit; those Friday positions carried the weekend to Monday. The kicker: those stranded trades made money, +$1,875 of price P&L, so the bug flattered the results. The honest same-day strategy is about $1,700 worse than the numbers above. The 21:00 trap is now a documented spec rule in our pipeline (same-day exits go at 20:55 or earlier), and it is a good reminder of why we audit our own rejections as skeptically as our wins.

What goes in the priors

Our flow-anomaly scoreboard now reads: concentrated flows leave residue, diffuse flows do not. The gotobi settlement flows and the London fix concentrate order pressure into minutes, and both left measurable out-of-sample edges. The session cycle spreads the same kind of pressure across entire trading days, and after costs there is nothing left to collect. Same physics at a different density, and the tradability flips.